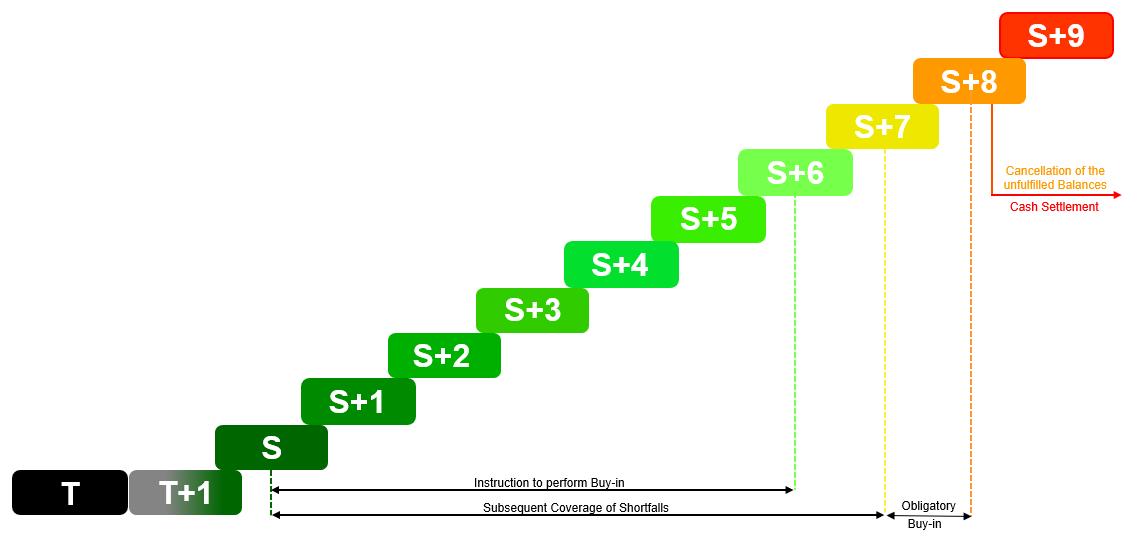

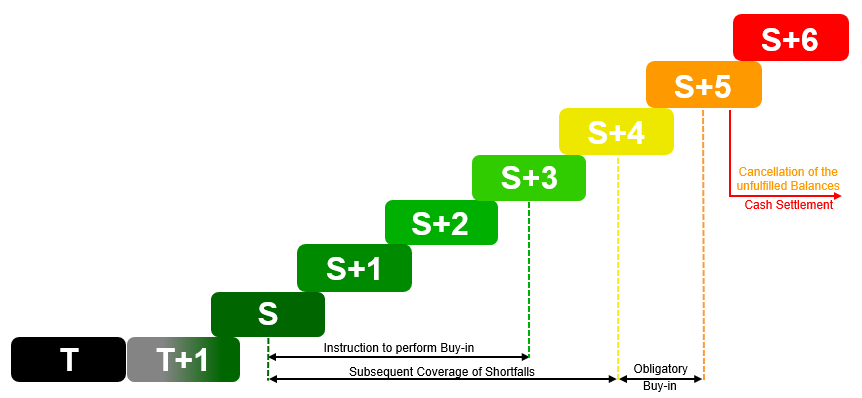

Settlement Period

The exchange transactions in CCP-eligible securities are to be settled on the second settlement day after the day of the business transaction (scheduled settlement day is T+2).

The settlement period comprises a period of two days between the trade date (T) and the scheduled settlement date (S).

If a participant fails to fulfil its delivery obligation on the scheduled settlement date, a default on delivery occurs.

Procedure in the event of a default on delivery

If CCPA has reason to believe that the default on delivery is not based on an insolvency or inability to render performance, that the default was not caused intentionally and that the Clearing Member will fulfill its obligations without delay, CCPA may declare a technical default.

In this case, the following actions will be taken in accordance with the clearing cycles listed below:

- Extension period

- Buy-in process

- Cash settlement

In case of a technical default on delivery, cash penalties are charged in accordance with EU law (CSDR).

All cash penalties resulting from CCP-eligible transactions concluded on the Vienna Stock Exchange are calculated and provided by OeKB CSD in accordance with the provisions of CSDR up to the time of settlement instruction fulfillment (the actual settlement day). These penalties will be collected from and distributed to the Clearing Members (affected by the settlement failure) by CCPA by means of aggregated PFOD instructions ("payment free of delivery").

Extended Clearing Cycle

The distinction to the longer clearing cycle is based on a longer extension period in accordance Article 37 Delegated Regulation (EU) 2018/1229 (RTS on settlement discipline) from S+4 to S+7 for the following financial instruments listed at Vienna Stock Exchange:

- other CCP-eligible equities, where the principal trading venue is located in a third country (Article 16 Regulation (EU) No 236/2012)

Download overview - other CCP-eligible securities (bonds, ETFs, certificates, warrants)

This longer extension period provides the Clearing Participants with additional settlement days to fulfill their delivery obligation, before a buy-in process is initiated. This contributes to significantly reducing the risk of cash settlements for our clearing participants, which leads to a general improvement of the settlement efficiency.